The economics, politics and political economy of UK-EU trade negotiations.

Mr. Gove’s ambition of signing a trade agreement by the end of 2020 reflects the government’s intention to avoid having to extend the transition period written into the Withdrawal Agreement. Under this, the UK would continue to abide by EU rules, including single market rules, until the end 31 December 2020, but without any of the rights that come with membership. The reason the transition period was written in was to avoid the economic disruption that comes with a sudden hard “Brexit” under which the UK and EU lose all preferential access to each other’s markets over night. The economic imperative clashes with the political cost of being perceived to be within the EU but without a voice or vote.

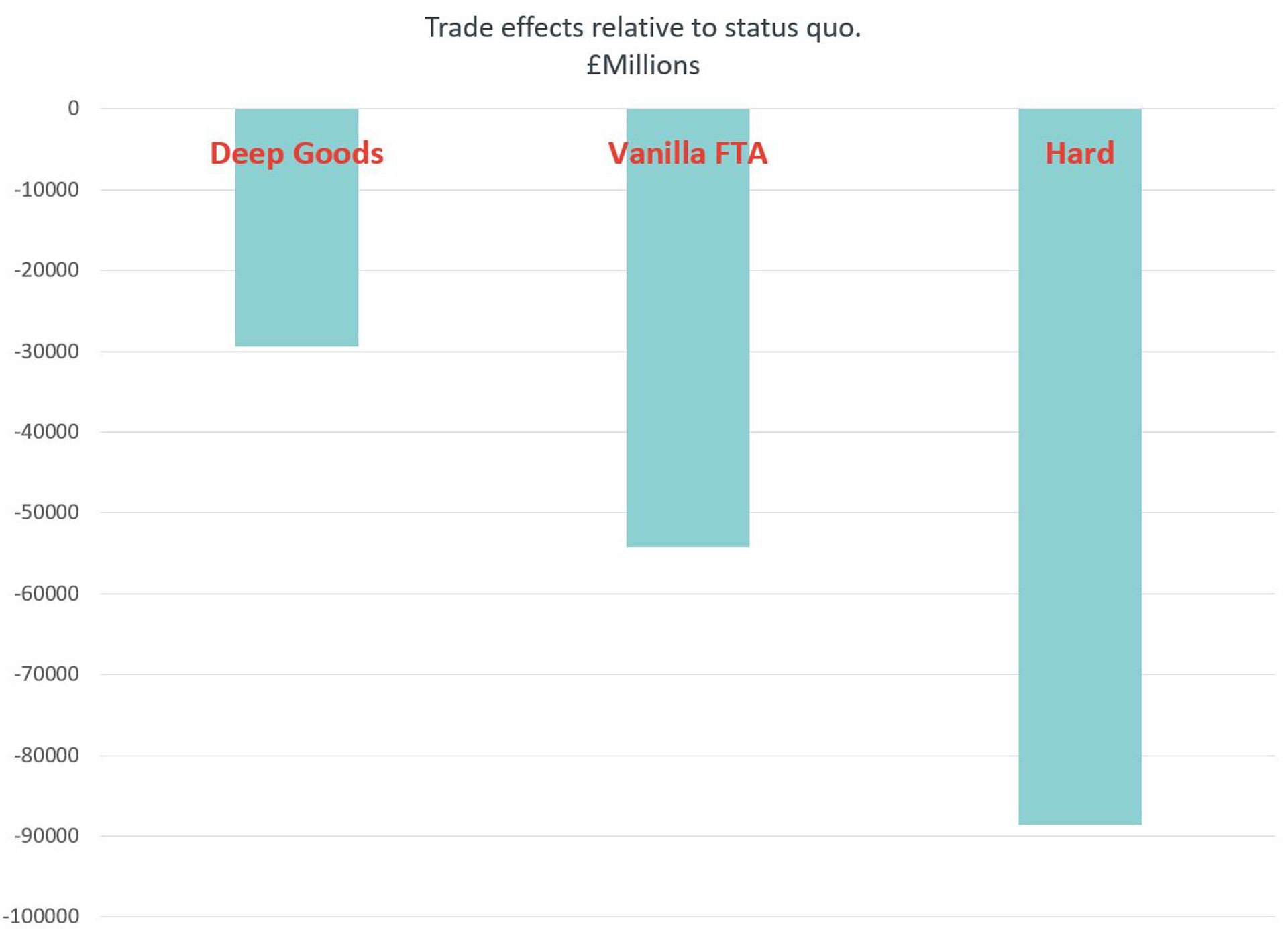

That tension may be set to last. This is because from an economic perspective, it is in the UK’s interest to negotiate a deep and wide-ranging free trade agreement with the EU. This is borne out by figure 1. The right hand column shows export losses per year under a hard exit i.e. without a trade agreement in place. The middle column shows losses under a relatively arms-length free trade agreement, like the one the EU has signed with Canada. The losses are still substantial. The left-most column shows losses under arrangements that uses as a starting point the agreement struck with the EU by Theresa May’s government in 2018. That agreement involves more comprehensive arrangements on goods, especially on regulation.

But here lies the rub: the deeper the agreement, the longer it takes to negotiate, let alone implement. Hence the probable need to extend the transition period beyond 31 December 2020, an outcome the European Commission has already contemplated. The government for its part has ruled out extending the transition period, which could increase the risk of a weaker agreement.

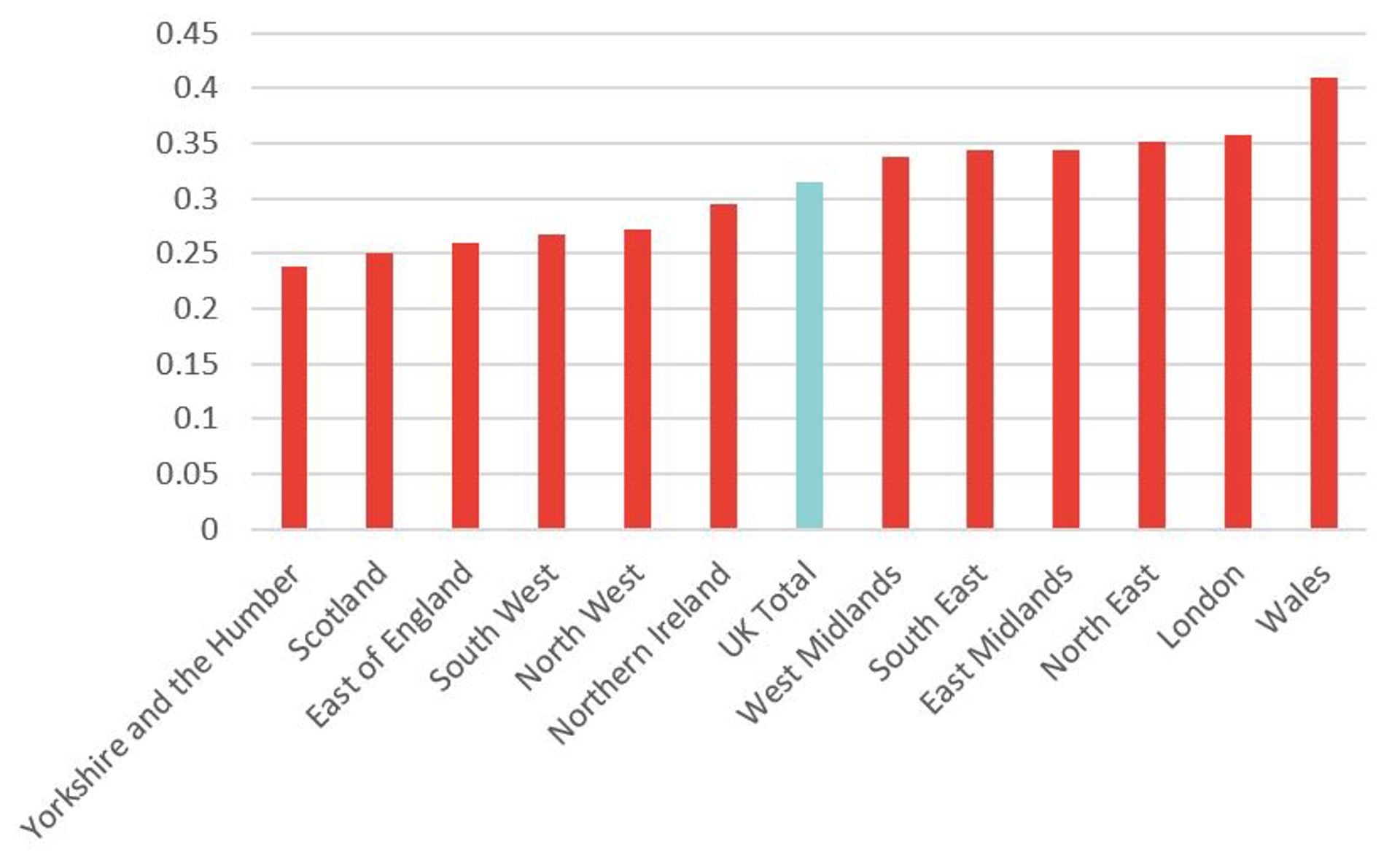

But pressure to find a deeper agreement may come from the political economy underlying the Conservative’s electoral win. Figure 2 shows the openness to trade (the ratio of trade to regional gross value added) of different regions within the UK. Crucially, the midlands, north east, and Wales (along with London and the South East) show higher degrees of openness than the UK average. For these three regions, this openness is driven by goods trade, with the EU the dominant partner (particularly in sectors like automotives). These three regions provided important parts of the political swing to the conservatives, and would be disproportionately affected by losses from a weaker FTA with the EU.

To this needs to be added the determination of the Scottish National Party (SNP) to seek another referendum on Scottish independence. The push for independence is likely to be greater the weaker the prospects for a deep future partnership are deemed to be.

Dealing with the wider world

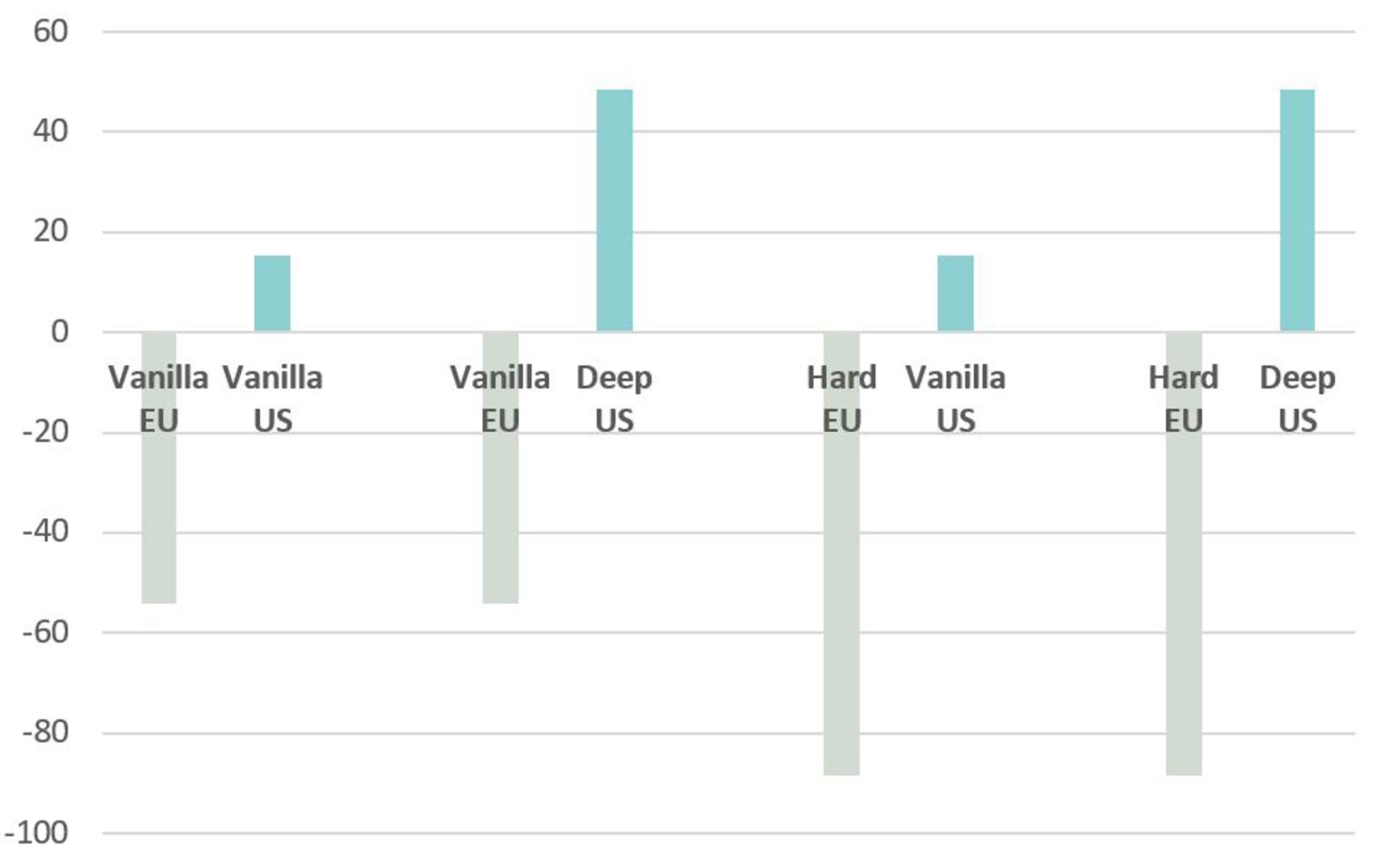

President Trump greeted news of the Conservative’s win with a promise that the US and the UK would soon agree a massive deal. He said this would be more lucrative than a deal struck with the EU. The underlying economics suggests this is very unlikely to be the case, unless the UK signs a particularly weak deal with the EU and replicates single market-type arrangements with the US (see Figure 3 below). Given that single market arrangements took decades to negotiate, this is unlikely to materialise.

Setting aside political rhetoric, the key challenge for the UK is that any negotiations between it and the US will be about regulation, whether in goods and services. The USTR’s negotiating objectives seek, notably, non-discriminatory market access in UK services sectors. Even if healthcare is excluded from negotiations, that leaves open the question of regulatory reforms in areas like audiovisual services and broadcasting, transport and finance. In goods trade, food and agriculture will be key issues.

But even before the UK seeks to strike a deal with the US, it would be well advised to secure deals with countries with which it currently benefits from a FTA by virtue of EU membership. In some cases the UK has negotiated replacement agreements. But in important markets such as Canada, Japan, Singapore and Turkey, this is not the case.

UK exporters therefore face a no-deal scenario with these markets. In Canada, for example, exports of motor vehicles, aircraft components and machinery face tariffs of between 6 and 9%. In Japan, the main issue is non-tariff measures that apply to these products.

Negotiating replacement agreements thus ought to be a priority for the UK government. The difficulty is that partners in question have little incentive to negotiate with the UK. This is because they can pocket such market access gains as they have via current arrangements with the EU for as long as the UK implements the EU’s customs code (i.e. as long as it is under transitional arrangements, and longer in the case of Northern Ireland under backstop arrangements).

For a fuller discussion and analysis, please see our article at the Trade Knowledge Exchange.