In the second article of our series on Covid-19 and UK higher education, we set out why any crisis in the higher education sector would be a blow to social equality.

Covid-19 will impact universities already struggling

UK universities, as shown in our previous article, are facing a potential Covid-19 crisis. With the pandemic likely to reduce overseas student numbers, a resulting fall in revenues will lead to ripple effects across the sector.

While the government released plans for grant extensions and low-interest loans at the end of last month, these would lead to higher costs in the future – and some institutions already struggling may not be able to bear the additional financial burden, if they are even able to access this finance.

The Institute for Fiscal Studies found recently that the likelihood of insolvency due to Covid-19 for higher education institutions depends more on their financial situation before the crisis, rather than on predicted losses from Covid-19.[1]

Our analysis shows that some universities appear financially vulnerable

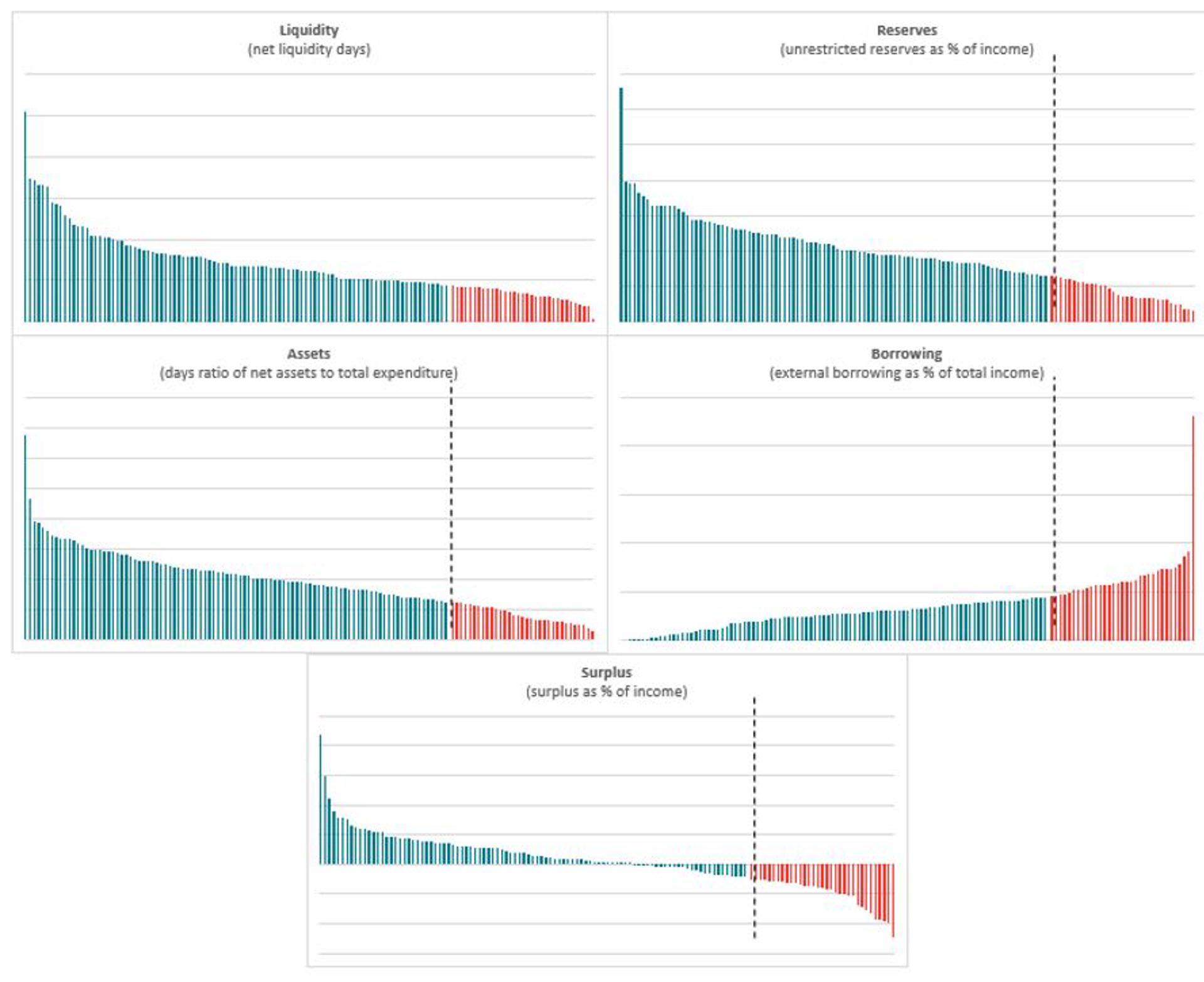

We’ve conducted our own analysis to understand which institutions appeared most financially vulnerable as the Covid crisis loomed. To do this, we’ve used five publicly available measures of financial stability: net liquidity days, unrestricted reserves as a percentage of income, ratios of net assets to expenditure, external borrowing as a percentage of income, and surplus as a percentage of income.[2] Figure 1 shows the distribution of these indicators across the sector.[3]

21 universities were found to be performing in the bottom quartile for at least three of the five indicators, and therefore appear, on this basis, to be financially vulnerable. Of these institutions, three are also heavily dependent on overseas fees, meaning they may be even more likely to struggle.[4]

Figure 1 Variation in financial performance across universities, based on HESA data

Source: Frontier Economics analysis of HESA finance data.

Note: Distribution of financial indicators across the sector, with blue bars representing universities ranked in the top 75%, and red bars representing universities ranked in the bottom 25%. The cut-off is shown by the black dotted lines. Values for each university are the simple average of the values across four years, from 2015/16 to 2018/19.

There are implications for social mobility

The majority of these vulnerable universities – 17 out of 21 – have a disproportionately high number of undergraduate students who previously studied at state schools or colleges.[5]

A number also offer access to a disproportionate number of students from low participation areas.[6] Across the UK, less than 12% of higher education students come from such areas, but several of the vulnerable institutions educate a much higher proportion from this group, outperforming benchmarks set for them[7] (as shown in the figure below).

The vulnerable universities, therefore, tend to be institutions that are actively promoting social mobility and contributing to government higher education access objectives.

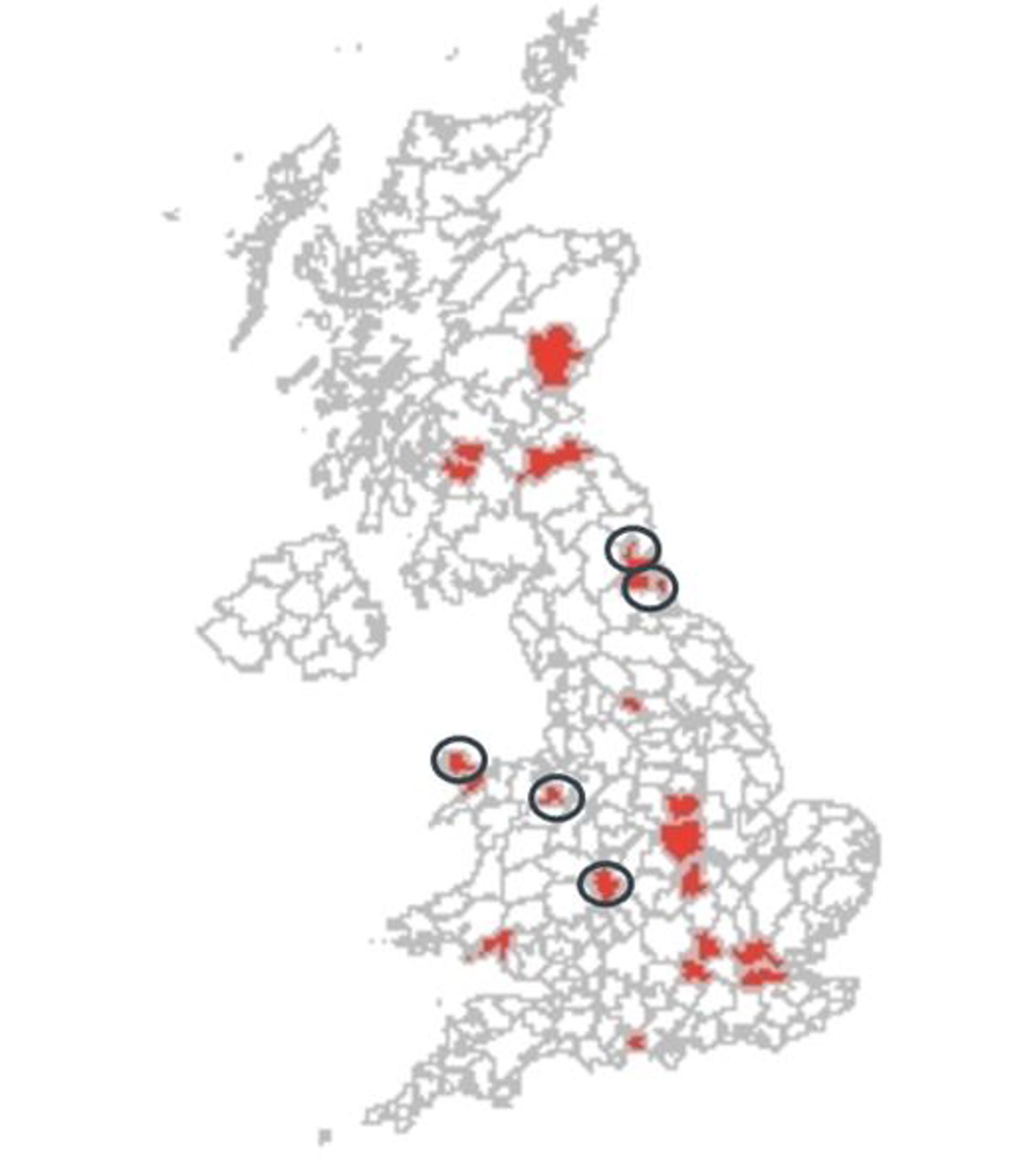

Figure 2 Contribution of vulnerable institutions to social mobility

Source: Frontier Economics.

Note: Travel to work areas that contain an institution in our list of 21 financially vulnerable universities are highlighted in red. The circles point to Travel to work areas with institutions which significantly outperform the national average in terms of participation from low participation areas as well as the benchmarks specifically set for them.

Analysis of HESA data shows that students from the local area of those institutions located in the North East, East Midlands and Wales are disproportionately likely to study in the same region, compared with the UK average. Any potential failure of universities in these areas is likely to disproportionately affect students from the local area, creating a risk prospective students in these areas may not go to university at all.[8]

Regional ‘levelling up’ will be affected

The 21 universities we’ve identified are located in 17 different travel to work areas (TTWAs), shown on the map above. While five of these are in London and the South East, the rest are spread across the UK, with the East Midlands, the North East, Scotland and Wales home to a disproportionate number.[9]

Any potential failure of these universities would be damaging to the government’s ‘levelling up’ agenda – especially given the chancellor’s recent budget commitment to increase R&D spending outside the ‘golden triangle’ of London, Oxford and Cambridge.

What’s more, universities contribute substantially to their local communities – not only through education but also through employment. Universities have been shown to increase GDP per capita in “close neighbouring regions” through direct spending (employment) and spillover effects[10].

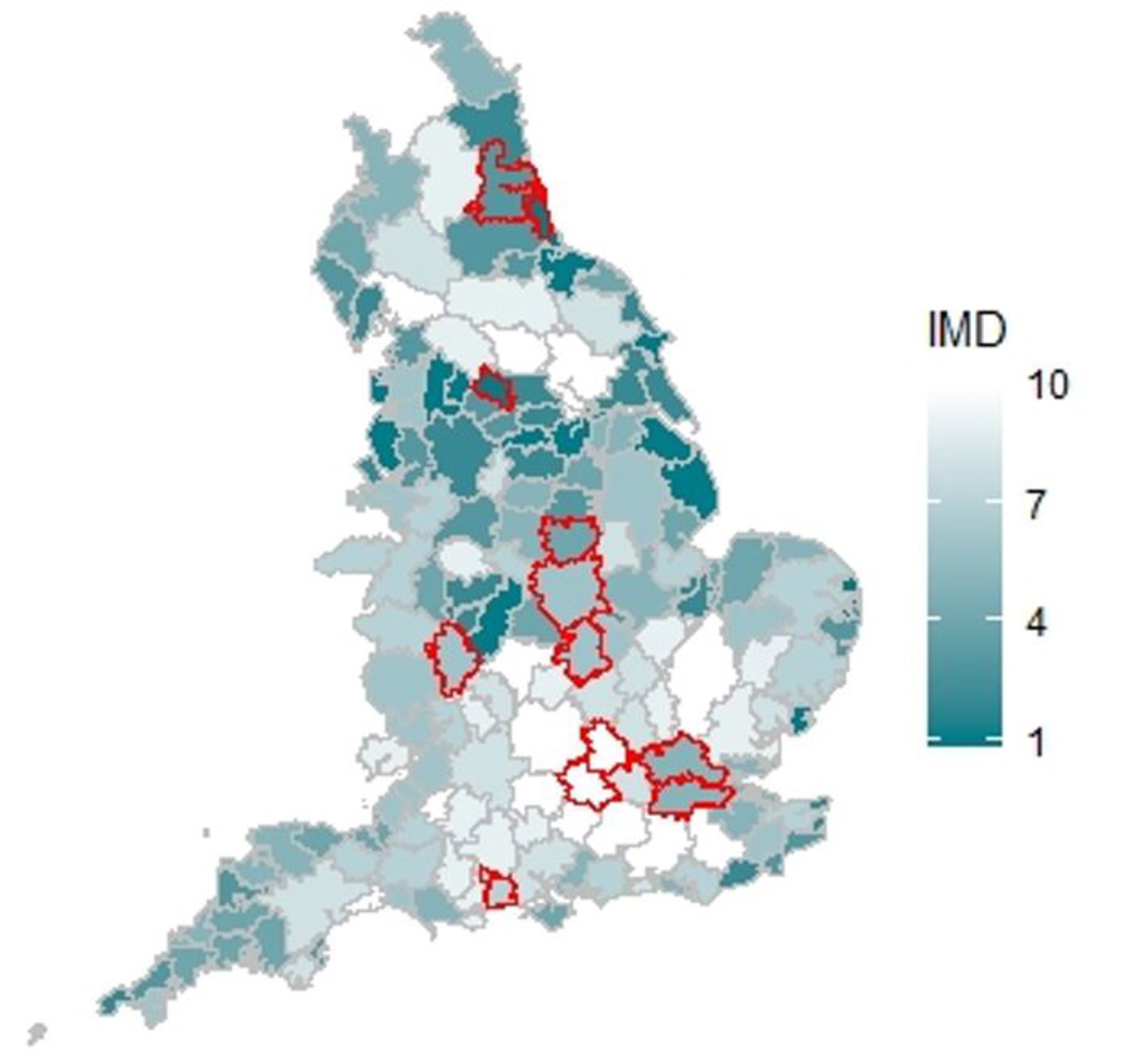

As the map below shows, some of the vulnerable institutions are located in areas ranking among the most deprived in England according to the Index of Multiple Deprivation. Any significant disruption of one of these local institutions would be particularly damaging for these communities.

Figure 3 Index of Multiple Deprivation ratings, overlaid with locations of financially vulnerable universities

Source: Frontier Economics analysis.

Note: Chloropleth map is based on IMD deciles, where the darker areas represent more deprived TTWAs. The IMD scores of the TTWAs are the weighted average of the LSOAs within them. The aggregated TTWA scores are then ranked and split into deciles. The red outlines depict TTWAs containing a financially vulnerable university.

Government refusal to bail out leaves few alternatives

As mentioned in our last article, the UK government has so far refused to offer a bail-out to the higher education sector.

Instead, it plans to offer grant extensions and low-interest loans – chiefly being rolled out in September – to cover a significant portion of the research funding gap left by the loss of overseas student fees.[11] This is capped, and only applies to non-publicly funded research activity – meaning it won’t cover teaching costs.

There will also be emergency loans available to universities on the brink of collapse, following a report by the IFS suggesting that 13 universities in the UK are in serious danger of insolvency.[12] These loans would give the government greater control over the management of the universities in question, from the subjects they teach to how much they pay their staff.

These are less than perfect solutions for universities. But without a bail-out, many may have no other option than to take out the loans on offer as emergency measures until they can once again attract international students.

For the universities we’ve identified, taking these government loans may be an additional financial burden that they simply cannot afford in the long term. As a result, they may be forced to combine loans with other drastic measures suggested by the government, such as closing university campuses or merging with other institutions.[13] This is if these universities are even able to access these emergency loans, as the decision is based on the restructuring plans which the institutions submit to the Higher Education Restructuring Regime Board, and the government has said that “not all providers will be prevented from exiting the market”.

Should it come to pass, all of this will change the shape of the university landscape as we know it. And, perhaps most crucially of all, universities that are important sources of mobility, access and local employment will be the hardest hit of all.

[1] Institute for Fiscal Studies, ‘Will universities need a bailout to survive the COVID-19 crisis?’, IFS Briefing Note BN300, 2020, https://www.ifs.org.uk/publications/14919.

[2] Analysis performed using HESA finance data from 2015/16 to 2018/19.

[3] The original version of this article named those universities that our analysis of HESA data indicated might be financially most vulnerable prior to the outbreak of Covid-19. The names of those universities have been removed upon request in order to ensure focus on the original intent of the article – to understand how financial pressures on the sector may have broader impacts on social mobility – rather than the identities of specific institutions.

[4] ‘Dependent on overseas fees’ is defined by the percentage of total income that comes from overseas fees, averaging HESA data across 2017/18 and 2018/19.

[5] When compared to the UK average state school intake of 90%. The result holds even when controlling for the subjects of study that are offered, entry requirements and the region in which each university is located.

[6] Measured using POLAR4, low participation areas are defined as middle layer super output areas (MSOAs) that are in the bottom quintile in terms of the proportion of young people who enter higher education at the age of 18 or 19.

[7] Benchmarks adjust the UK average to take into account the subjects of study available at the institution, the entry requirements, and the region of domicile.

[8] Analysis uses HESA data for the 2018/19 academic year.

[9] Disproportionate in terms of the proportion of universities in that region that are among the 21 less financially stable.

[10] Valero, A., Van Reenen, J., (2019), The economic impact of universities: Evidence from across the globe, Economics of Education Review (68)

[11] Department for Business, Energy & Industrial Strategy, University research support package: explanatory notes, June 2020, https://www.gov.uk/government/publications/support-for-university-research-and-innovation-during-coronavirus-covid-19/university-research-support-package-explanatory-notes

[12] ‘Emergency loans for universities about to go bust’, BBC News, https://www.bbc.co.uk/news/education-53429839.

Authors

Alex focuses on climate change and decarbonisation. She uses her analytical skills to help solve problems that relate to the electricity market, transport sector and fuel supply.

View profileUK higher education and Covid-19

Read our first article in the series, which explores the fall in overseas student numbers.

Discover more